Every time a customer pulls out a credit card from a megabank or fintech, your community financial institution loses more than interchange income. You lose visibility into spending and, over time, part of the relationship. Credit cards are becoming too important for community banks to ignore.

For years, card issuing looked out of reach with too much required infrastructure, compliance, and too many moving parts. But things have changed with technology and modern processes.

The expectations from customers are clear. They want credit cards to fit seamlessly into their digital banking experience. And if they don’t get that from you, they’ll get it somewhere else. Research shows that one in three U.S. customers changed banks in 2025 because the digital experience didn’t measure up.

Why a Digital Credit Card Program Matters More Than Ever

Community banks succeed on relationships, not scale. In today’s environment, those relationships are shaped less by branch visits and more by mobile screens. The credit card is one of the most visible and frequent touch points you have with customers.

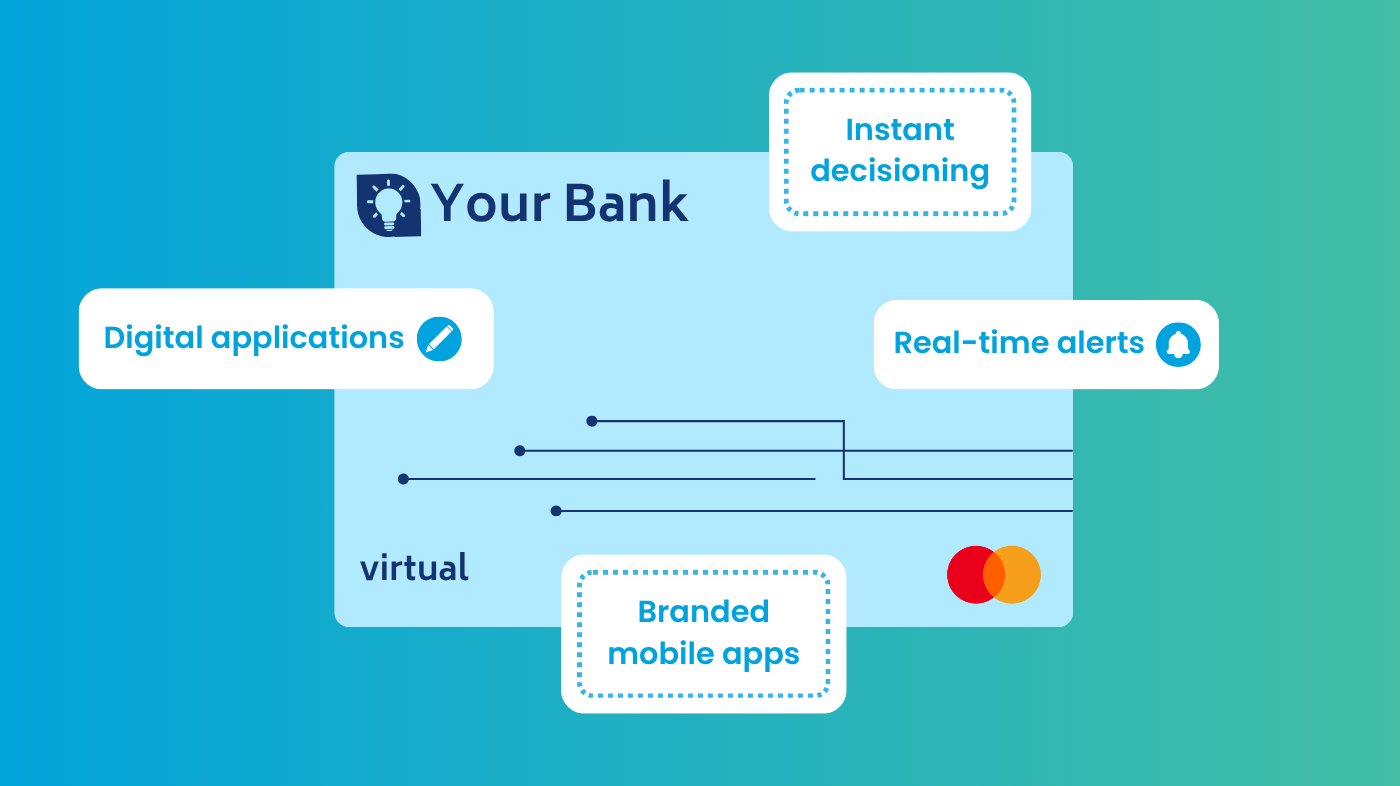

That’s why the digital side of issuing matters. Features that were once “nice to have” are now expected:

- Digital applications that let customers apply on their own schedule

- Instant decisioning so they’re not left waiting

- Mobile wallet compatibility with Apple Pay, Google Pay, and Samsung Pay

- Bank-branded mobile apps with modern, easy-to-use interfaces

- Real-time alerts and spend controls for peace of mind

- Commercial credit tools like role-based permissions, mobile-first expense reporting, and integration with accounting systems such as QuickBooks

When your customers can do all of this through your bank’s brand, you stay at the center of their financial lives.

The Choices for Community Banks

Community banks generally face three options when it comes to issuing credit cards:

- Outsourced agent programs get you into the market quickly but often put someone else in full control. Revenue and data usually stay with the provider.

- In-house self-issuing gives you complete control, but the time, cost, and staffing requirements are often out of reach for smaller institutions.

- Hybrid issuing platforms combine the best of both approaches. You keep your brand, your income, and your data, while a partner handles the complexity behind the scenes.

For most community banks, the third option has become the most realistic way forward.

How CorServ Enables Digital Banking

At CorServ, we’re helping community banks compete directly with large national issuers. Our platform makes it possible to:

- Launch a fully branded credit card program in as little as 90 to 120 days

- Offer digital applications and instant decisioning to meet customer expectations

- Deliver mobile apps and modern interfaces that make card management simple and engaging

- Provide mobile wallet integration across Apple Pay, Google Pay, and Samsung Pay

- Support commercial clients with advanced features like dynamic credit limits, role-based employee controls, and accounting system integration

- Maintain ownership of program income, credit decisioning, and full access to data

The goal isn’t just to check a box on your product lineup. It’s to create a competitive advantage that strengthens loyalty, drives revenue, and keeps your bank top of mind.

The Bottom Line

The digital revolution in card issuance is no longer on the horizon. It’s already here. Community banks that move now can win back wallet share, retain customers who are being targeted by fintechs, and create new income streams.

Customers don’t just want a credit card anymore. They want a digital experience that works with mobile apps, mobile wallets, and digital instant notifications that give them control. The good news is you don’t have to build it all yourself. With the right partner, you can offer a program that looks and feels like it was built in-house, while staying focused on what community banks do best: serving customers and building relationships.