Credit card issuing can be one of the most powerful growth levers for a community bank. Done right, an issuing program generates non-interest income, strengthens brand visibility, and builds loyalty in a competitive market.

For many banks, the common entry point is the Agent Program. These arrangements make it simple to offer cards to customers. The agent provider manages underwriting and servicing, and the bank collects a modest referral fee. But that simplicity comes at a price, with thin revenue, no control, and weaker customer connections.

There’s a better path. An Owned Credit Card Program allows banks to capture the economic and strategic benefits of issuing without the burden of building systems or staffing every role internally. With the right partner, community banks can own their program while outsourcing the most complex operational tasks.

The Agent Program: Simplicity with Significant Trade-Offs

Agent programs function as referral models. The agent bank controls every element of the program including credit decisions, product design, and customer service. This makes them appealing for banks that want the easiest possible path:

- Low operational demand – The agent bank manages all tasks including marketing, so the bank avoids training any staff about the program.

- Fast time to market – Programs can be launched quickly, letting banks offer a credit card without lengthy preparation.

- Reduced oversight – Since the agent makes all credit decisions, the bank carries less direct risk, except on guaranteed accounts.

But the trade-offs are substantial:

- Minimal financial return – Community banks in Agent Programs keep limited program revenue. The majority of the interchange, interest income, and fee revenue flow to the agent bank instead.

- Loss of control – The bank has little or no input into underwriting, credit limits, marketing, servicing or product features. This leaves the program disconnected from local market needs.

- Credit risk without reward – In some programs, banks guarantee accounts for their customers. That means they may share in losses while receiving little to none of the upside economics.

- Limited customer access – Without transaction and performance data, banks cannot cross-sell effectively, identify trends, or build stronger relationships.

- Innovation bottlenecks – Standardized vanilla card products make it hard for banks to compete with custom rewards, commercial card solutions, or digital features like virtual cards.

What begins as an easy solution often leaves banks tied to someone else’s program with someone else’s profit.

The Owned Program: Control and Profit with the Right Support

An Owned Credit Card Program changes the dynamic. Instead of giving up revenue and customer relationships to a third party, the bank retains ownership of its portfolio while relying on an experienced partner to manage regulatory and operational complexity.

With this approach, community banks can:

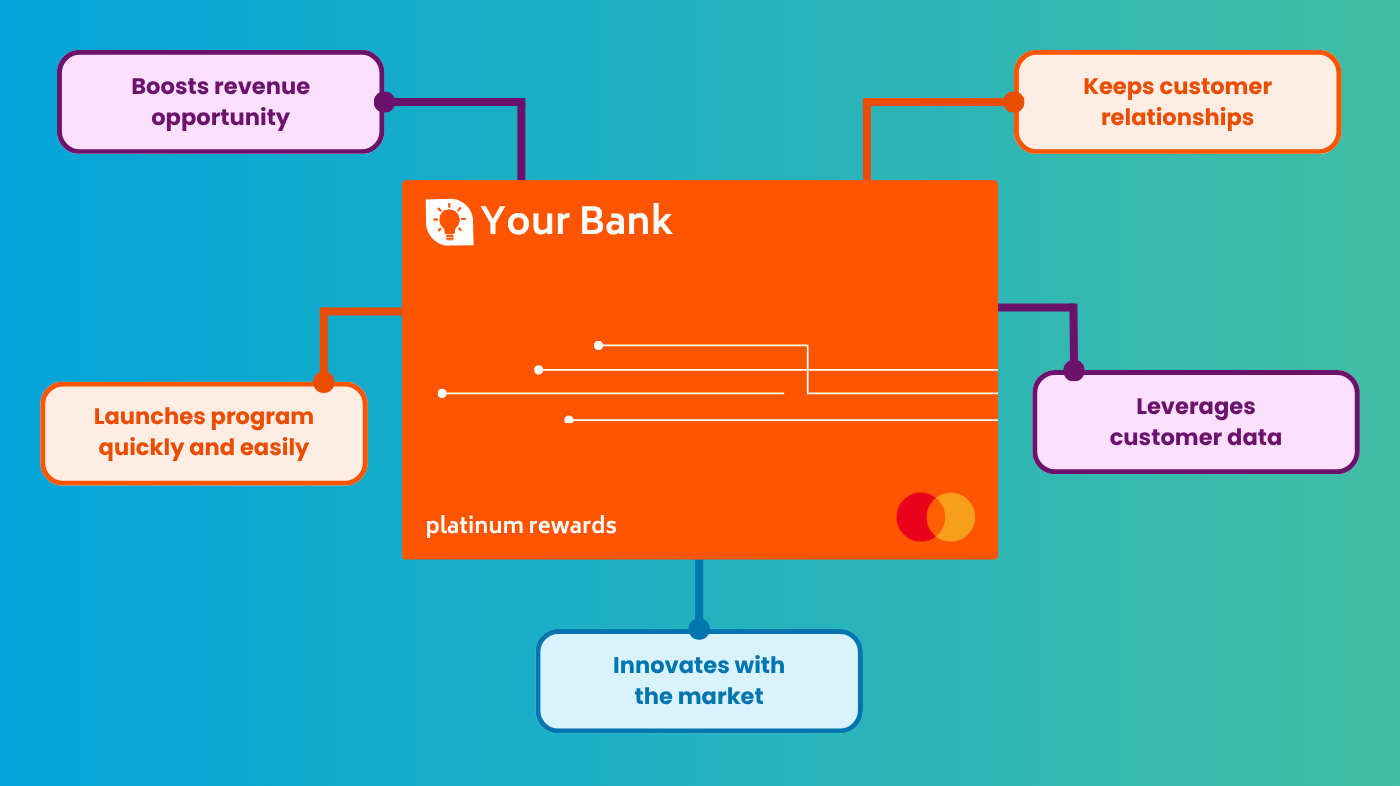

- Keep the economics – Interchange, interest, and fee income remain with the bank, often producing double-digit margins without building a program from scratch.

- Apply local knowledge to credit decisions – By setting or influencing credit policies, banks can leverage deposit history and customer loyalty to make more effective lending choices.

- Deepen customer loyalty – The bank’s brand stays at the forefront, and access to customer and transaction data allows for meaningful cross-sell and engagement.

- Launch quickly with less friction – A turnkey partner can handle compliance, fraud, servicing, and network integration, getting banks live in as little as 120 days.

- Stay competitive over time – Owned programs allow for ongoing innovations, such as commercial cards, virtual cards, tailored rewards, or advanced spend controls.

This model gives banks both profitability and flexibility while eliminating the burden of building every operational layer in-house.

Why Ownership Matters

Agent Programs provide convenience and speed, but they limit revenue, dilute control, and may even leave banks exposed to credit risk without adequate return. Owned Programs put profit, customer data, and decision-making back in the hands of the bank while outsourcing the most complex operational tasks to an experienced partner.

The choice between an Agent Program and an Owned Program is strategic. It determines whether a bank is simply a referral partner or the true owner of record. When making your decision, ask these questions:

- Do you want to settle for referral fees or build lasting non-interest income?

- Do you want other providers setting credit limits for your best commercial customers?

- Do you want to give up the ability to align with your community’s needs?

- Do you want limited visibility into customer behavior or actionable data that drives growth?

- Do you want to stuck with basic functionality or compete successfully leveraging ongoing innovations?

Owning your credit card program ensures that it strengthens your bank’s brand, profitability, and customer relationships, not someone else’s.