Overview

Many community-based U.S. financial institutions (“FIs”) are facing a weighty dilemma.

How do they meet demands from their Board of Directors to more aggressively grow loan and fee-based portfolios while providing quality products and services for their customers and members, now that the economy is back on the upswing?

Few likely consider expanding their credit card program as a source for this growth, since the majority of community FIs have either exited the credit card industry or exist on its margins, as a participant in a credit card program owned by a larger bank that owns and manages the loan portfolio.

But that is exactly where they should be looking, thanks to an innovative business model from CorServ Solutions that offers turnkey yet customized credit card solutions. A typical CorServ client is an FI that wishes to offer or expand its credit card product to its relationship consumers and businesses, while controlling the customer experience at every key touch point.

This scenario was typically not available to FIs who entered into agent bank relationships with major credit card providers, thereby ceding control over decisions being made regarding their credit card portfolios. In agent bank arrangements, the local bank does not underwrite, fund or keep the credit card balances on its books. Importantly, it has little or no say in the issuing bank’s decisions to cancel a card; and if it guarantees the loan, it takes all the risk and receives no incremental reward or revenue.

Moreover, agent banks generate limited income to the community banks that participate. And the inability to leverage valuable customer relationships can create potentially expensive problems and reputational risk for the FI when high-value cardholders have a question or concern.

Nevertheless, thousands of banks and credit unions are part of agent bank credit card programs because they are unaware of better options available for them. Thanks to CorServ, the playing field has dramatically changed.

FIs who participate as agent banks or who have exited the credit card market altogether should now reconsider their options. The ongoing economic recovery coupled with federal and state regulators desiring to see more balance sheet diversification have presented community-based FIs with an attractive opportunity … the ability to participate in a CorServ credit card

Account Issuer Program that enables them to capitalize on their strong relationships with customers (banks) or members (credit unions), own the loans and thereby enhance their profitability.

CorServ’s Officers – credit card industry leaders who have decades of experience and expertise – have implemented new technology advancements and comprehensive turnkey services that mitigate the risks, accelerate the time to market and increase the financial rewards of owning credit card loan portfolios, which typically outperform other income-producing FI assets. Importantly, CorServ’s goals, policies and pricing structure align with the institution’s own objectives and requirements.

This white paper examines the pros and cons of participating in a CorServ credit card Account Issuer Program versus utilizing an agent bank or sitting on the credit card sidelines during this dynamic, post-Recession era.

Upon reading it, FI Officers should be able to answer this pertinent question: Which credit card strategy should my FI employ?

The Good Old Days … and Change

The credit card industry enjoyed a 40-year history of dynamic growth. Perhaps no era was more mercurial than the 1980s, as further growth was spurred by the elimination of state usury restrictions and the introduction of annual fees, which led to a doubling in the number of credit cards in use. Consumers’ credit card balances increased more than five-fold by 1990 and FIs issuing credit cards enjoyed soaring profits.

Competition, more robust consumer data analysis and the threat of additional federal legislation that would cap interest rates led to the introduction of a wide variety of sophisticated credit card pricing strategies and offers, and unprecedented consumer usage and industry profits. Thousands of FI’s and retail businesses issued millions of credit cards and consumers and businesses alike utilized them.

But the Great Recession burst the credit card bubble. While its official length was only from December 2007 to June 2009, some of its ill effects lingered much longer. The rate of defaults on credit cards and other forms of unsecured lending led to record high credit card charge-off levels, prompting credit card issuers to alter their credit risk models and to cut nearly $2 trillion from existing lines of credit.

Further prompting some banks to exit or limit participation in the market was the Credit CARD Act of 2009, which restricted the ability of FIs to unilaterally increase the annual percentage rate, fee or finance charge on an existing (outstanding) credit card balance except in certain instances, e.g., promotion rates with terms of at least six months, variable rate cards that adjust with changes tied to external indexes or if payments are more than 60 days late.

This industry-wide scaling back led many FIs to exit the credit card industry altogether, and today just 55% of credit unions and 19% of banks2 have credit card loans on their balance sheet. Instead, many participate in agent banking relationships orchestrated by a handful of major banks – which fail to leverage and build on the strong relationships that community- based institutions have with their customers.

Many FIs with strong balance sheets have been deterred from entering the credit card marketplace or “upgrading” from agent bank-based relationships to participating in issuer bank programs. The reasons for maintaining the status quo or remaining on the credit card sidelines are many, and – in most cases – these barriers to entry were once understandable:

- Time to market – If an FI wanted to become a direct issuer, it required assembling the necessary resources (e.g. staff, technology and suppliers) to handle back-office processing, servicing, marketing and risk management.

- Financial capital – Constructing the infrastructure to design, build, manage and process a credit card operation could have required a significant capital investment.

- Human capital – Most community-based FIs have typically had few employees in management with hands-on experience in the credit card industry.

- Risk Management – Often, FI leadership have had understandable concerns with managing the risk associated with credit and fraud losses, credit policy and strategy, and relationship-based pricing.

- Marketing – Many FIs were challenged to implement best practices in credit card product design, pricing, rewards program management, account acquisition marketing, and channel management. They also lacked the resources and expertise to pursue life cycle marketing, including activation and retention strategies.

- Technology infrastructure – FIs with little credit card experience may have had concerns about their ability to manage customized credit card technology and related costs – including origination, credit decision making, processing, sales/servicing, data warehousing, acquisition, rewards and other components – to integrate seamlessly with its existing IT infrastructure. Also, some FIs have struggled to balance credit card-specific IT requirements with other technology priorities.

- Profitability timetable – Finally, after struggling through some lean post-Recession years, FIs – realizing that a new or updated credit card program may take three or more years to recover the investment required and turn profitable – may have been more inclined to turn to simple “quick fix” projects and programs in an attempt to reap rewards more rapidly.

Why Now? What’s Changed?

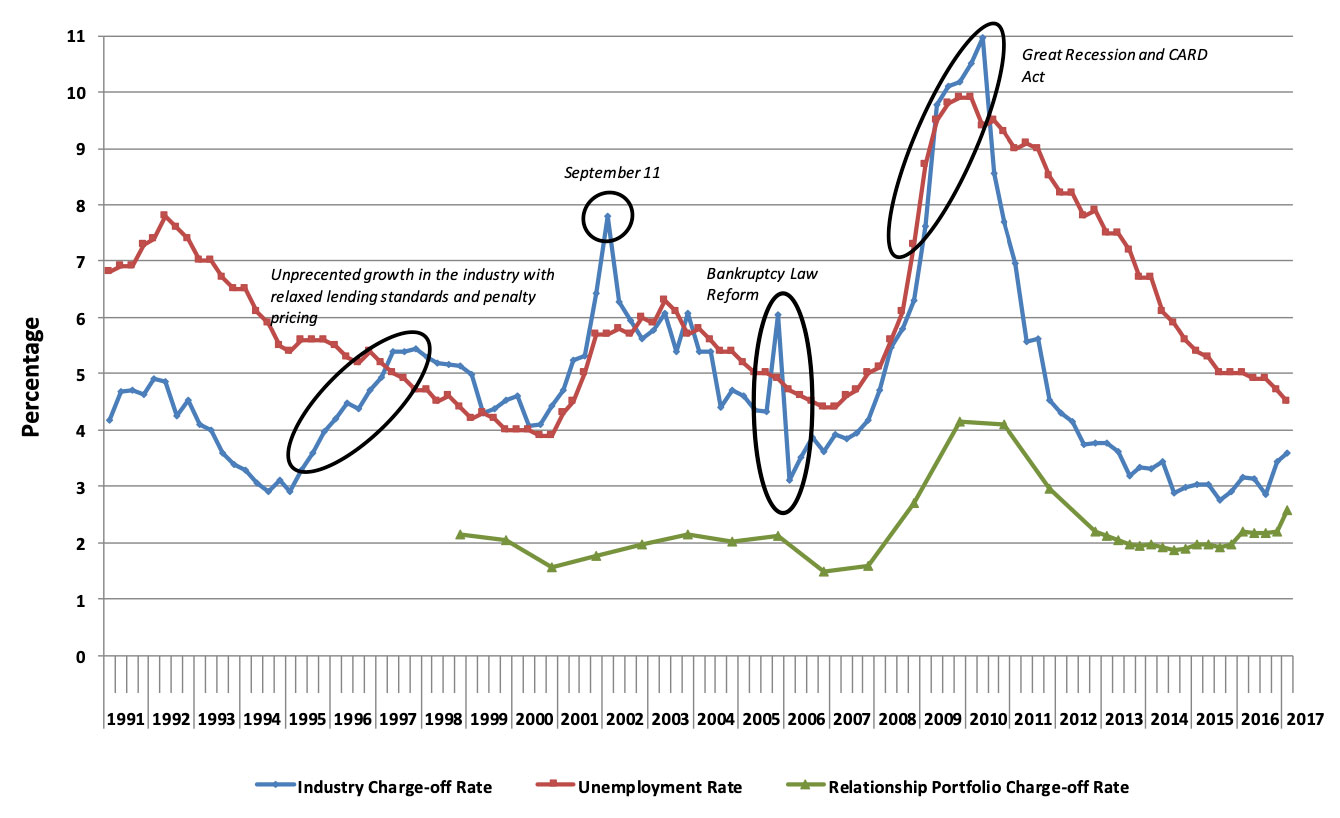

The ongoing economic recovery from the Great Recession has, at last, opened the doors of opportunity for many banks and credit unions. The industry has stabilized, as evidenced by the industry-wide decline in charge-off rates to 3.5% for all U.S. issuers, which coincided with a similar drop in unemployment.3

Data Sources: St. Louis Federal Reserve for Industry Charge-off Rates, NCUA for Relationship Charge-off Rates and Bureau of Labor Statistics for Unemployment Rate

Interestingly, charge-offs on relationship-based portfolios worsened during the Recession, but never as precipitously as the overall industry experienced. Community FI credit card losses peaked at just over 4.0%, well below national issuer portfolios, and today are back to pre- recession levels of 2.0%, further justifying what FI executives already know – relationships are a key to success for community-based FIs.

The Board of Governors of the Federal Reserve confirms the profitability of the credit card industry, indicating in its most recent annual report to Congress that “credit card earnings have been almost always higher than returns on all commercial bank activities.” For instance, in 2013, the average return on all assets, before taxes and extraordinary items, was 1.52 percent – compared to 5.20 percent for credit card banks.

That is wonderful news for FIs seeking to broaden their portfolios, further leverage their relationships with customers, and invest in an enterprise that can build high-quality and profitable assets and services. It may also help explain why both the January 2014 and April 2014 Senior Loan Officer Opinion Surveys (SLOOS) found that more lenders have loosened lending standards, thus increasing the overall credit supply.4

But those metrics alone do not sidestep the aforementioned barriers to entry in the credit card marketplace. Fortunately, some other changes do manage to overturn those impediments, offering community-based FIs – at last – the opportunity to re-enter the credit card business by participating in CorServ’s Account Issuer Program.

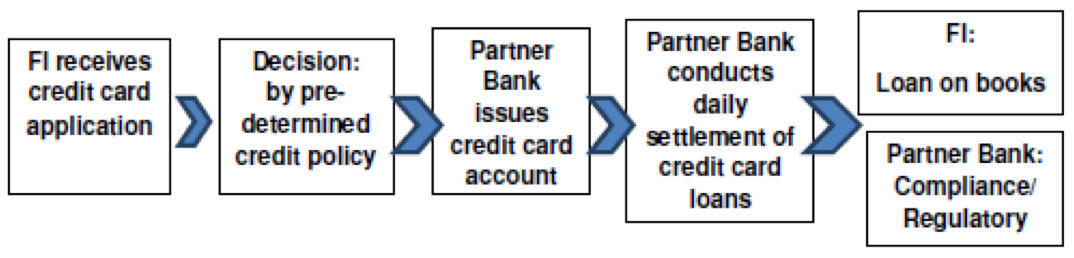

CorServ’s Account Issuer Model

![]()

This new credit card era can offer forward-thinking FIs the opportunity to overcome one-time barriers to entry and participate more actively in the revolving credit arena.

The development of turnkey credit card issuing solutions by CorServ Solutions has virtually eliminated or extensively mitigated those obstacles. By establishing a network of strategic partners with expertise in the vital functions necessary to operate and manage a credit card portfolio, CorServ enables FIs to obtain bundled services that cover credit card issuance, processing, servicing, program management, technology, compliance, credit policy and strategy, fraud and more.

Time to market is overcome because the FI can leverage an existing platform designed with competitive and compliant credit card products ready for issuing.

Similarly, the needs to attain the required financial capital to build an infrastructure and the human capital to manage it are in place and ready for your FI to leverage. With CorServ, the institution will not need to make capital purchases or add full-time equivalents to the payroll. Also, risk management concerns are eased by CorServ’s establishment of proven credit policy and strategies through a franchised-type approach to credit card portfolio management, as well as the additional assumption of fraud risk – as CorServ shares responsibility for possible losses.

Perhaps one of the most insurmountable barriers in the minds of many FIs is the need to develop a robust technology infrastructure in order to manage all aspects of credit card origination, decision making, processing, sales/servicing, data warehousing and management. That problem, too, is eliminated by outsourcing those activities via CorServ, which has assembled an extraordinary technology team who offer not only the key services but also the platform for seamless integration with the FI’s existing systems.

As for the growth and profitability timetable, CorServ aligns its own compensation to the portfolio’s performance. That mutual incentive, hastened time to market and limited capital investments have some CorServ programs cutting the time to achieve monthly profitability to as little as six months and cumulatively within one year.

What all this means is – at last – a bank or credit union can leverage its existing, locally-earned customer or member relationships and further strengthen trust and loyalty by offering a robust suite of credit card products at a fraction of the risk.

Banks can sell a credit card to customers at a fraction of the cost of someone else from the outside; they know them better, and can give them better products.

A Strategic Business Opportunity

Nobody knows its customer/member better than the local community bank or credit union. So it is important to partner with a practitioner like CorServ that appreciates the value of capitalizing on the relationships the FI has forged and the reputation the institution has earned through its investment in the community. That means retaining the ability to control the customer/member experience through all phases of engagement and across all lines of business.

The best option for most FIs interested in owning customer generated credit card loans is to participate in CorServ’s turnkey Account Issuer Program, which enables the institution to cost- effectively enter the credit card business by offering a full range of consumer, small business and corporate credit card products and services as complimentary and embedded products for existing customers. In doing so, the FI owns a high-yielding diversified asset that can be launched in less than 120 days from contract, risks are managed, the FI maintains control over credit decision making, revenue and profits are maximized through loan portfolio management and ownership, and each branch can have online and telephone access to support staff should questions arise.

FIs that remain hesitant to invest in CorServ’s Account Issuer Program may wish to pursue other ways to provide their customers with credit card offers such as becoming a direct issuer. CorServ can help FIs create a custom solution.

What You Need to Participate in CorServ’s Account Issuer Program

With the barriers to entry overcome and the economy finally on the upswing, many FIs are deciding to enter the credit card business as active participants in a well-structured Account Issuer Program with CorServ. Doing so propels them into a profitable business, but in lock-step with a knowledgeable and experienced practitioner who can help them navigate unfamiliar waters.

With the right network of CorServ-managed partners, FIs can aggressively enter, compete in and profit from the burgeoning credit card marketplace, while effectively managing risk. Here are some functional areas FI’s will optimize with CorServ to enable an efficient, well- managed and profitable credit card program:

- Determination of a credit card strategy – In creating the program, CorServ works with the FI to set goals and parameters for a comprehensive credit policy and strategies that optimize FI control of the decision making process. They collaboratively establish score cutoffs, debt to income ratios, relationship values and other criteria so that even automated decisions reflect the policies and priorities of the FI.

- Establishing a multi-year financial plan – CorServ will work with FIs to establish a long- term financial plan designed to meet its strategic objectives while addressing risk management criteria, including credit, collection and fraud exposures. Significantly, CorServ will share in the responsibility for fraud-related financial losses.

- Understanding and agreeing to all support requirements – These days, a strong Account Issuer Program limits the FI’s need for dedicated personnel to operate or manage the portfolio. CorServ has the resources to handle accounting/settlement, risk management, technology infrastructure, product development, compliance and customer service functions to the FI’s level of satisfaction, and is willing to align its compensation system with the FI’s.

An Ideal Partnership

An ideal partnership should coordinate the interests of all parties and work effectively according to the following parameters:

Rousing Successes

Rousing Successes

Many large FIs have recently earned significant returns from their renewed interest in credit card lending, and have a positive outlook for the future, according to a Federal Reserve study.6 That optimism has been fueled by more robust credit card loan portfolio growth. Large issuers – including JPMorgan Chase and Capital One Financial Corp. – have in early 20147experienced double-digit increases in card sales volume.

Community-based FIs are beginning to experience similar successes, especially those participating in programs that leverage the right strategic partner(s) for limiting the risk while reaping financial rewards. Some are using their new-found shared control in the decision- making process to specifically target new and potentially-profitable audience segments.

For instance, some FIs are reaching out to Generation Y (or millennial generation) consumers, who are much more comfortable with online banking than their forbearers, and receptive to customized online or mobile marketing programs that address their needs.

Experts are anticipating that credit unions will aggressively expand their focus on credit cards, given the industry’s modest growth rate since the Recession. According to one industry observer8, “With credit cards’ high relative rates, nearing commodity in terms of features and low switching costs, one could argue there is no reason every member household shouldn’t have a card.”

In fact, today 77% of U.S. consumers carry one or more credit cards9. So, why shouldn’t a community-based FI’s customers be carrying the credit card of their primary/local financial institution?

Next Steps

Among the many lessons learned from the Great Recession is that FIs must have the mindset and infrastructure in place to anticipate, adjust to and react to economic and marketplace challenges or opportunities.

As this white paper has illustrated, now is the time to proactively assess an FI’s willingness and ability to aggressively but prudently re-enter the credit card marketplace.

CorServ Solutions Inc. is a leading provider of credit card issuing solutions and support services for banks and credit unions. To learn more about the CorServ Account Issuer Program and other innovative credit card solutions, visit www.corservsolutions.com; or call 404-939-6949.